Q1 2026 Private Markets Outlook

Strategy Snapshot

Our key perspectives for each Private Markets Strategy

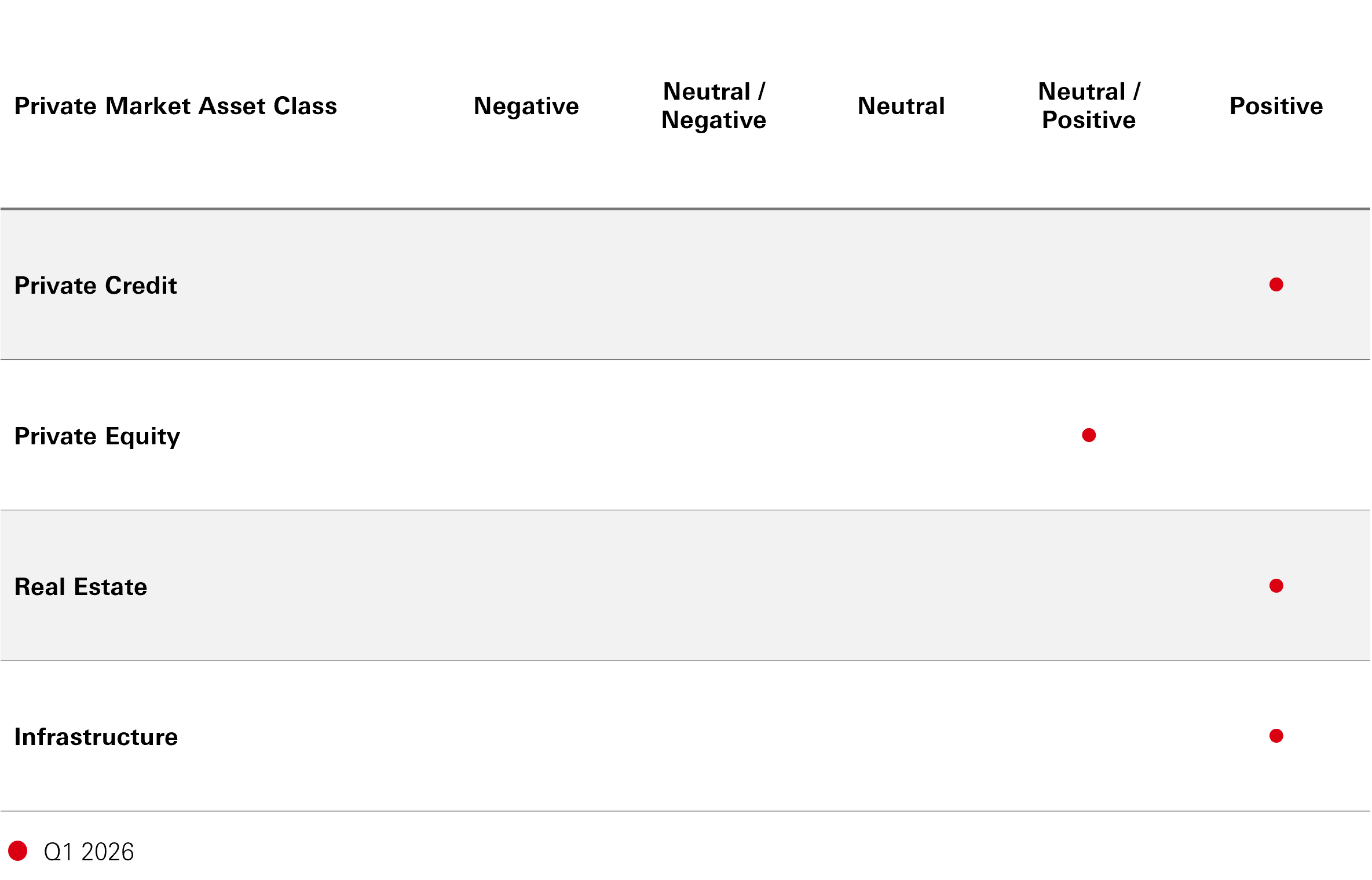

Proposed Strategy Views

In our view, the opportunity set for Private Market strategies remains deep. Within the sub-sector of Private Credit, we continue to hold a ‘Positive’ outlook.Investor appetite for private credit remains strong, thanks to its stability, yield premium, and consistent income, but deployment challenges and rising regulatory scrutiny are shaping the landscape. While the incidence of defaults is low, moderate credit deterioration is expected. However, lender flexibility and potential rate cuts in 2026 could support deal activity and should position experienced investors for compelling, risk-adjusted returns.

We maintain our stance on Private Equity at ‘Neutral Positive’. We continue to have a cautiously optimistic outlook as falling interest rates and resilient equity markets boost exit activity, especially within technology and healthcare, while lower financing costs support buyouts and refinancings. We remain cognizant of uncertainty emanating from delayed economic data in the US, as well as ongoing policy and geopolitical risks which may pose challenges for dealmaking and future rate decisions

In Real Estate, we continue to hold a ‘Positive’ outlook for the asset class. Higher property yields and steady rental growth—driven by limited new supply and tenant demand for prime assets—support total returns, though elevated interest rates keep risk premiums tight.

Digitalisation and electrification are driving infrastructure investment, with US electricity demand expected to rise sharply due to industrial, data centre, and transport electrification. Investors are targeting both established areas—like grid upgrades and renewable energy—and emerging sub-sectors such as electrified transport, data centre power solutions, and repowering older assets, all of which offer strong potential for value-add returns. As such, we remain ‘Positive’ on the outlook for Infrastructure.

Source: HSBC Alternatives, as of December 2025.

Our Asset Class Views

Private Credit

Positive

Review of Q3 2025

Although the immediate turbulence from tariffs and Q2 volatility has subsided, its ripple effects persisted into Q3. Private credit–financed deal activity in the US market slowed, with deal count and volume down roughly 13 per cent year over year. With fewer deals supporting buyouts and M&A, the imbalance between demand for private credit and available supply has deepened in recent months. In contrast, stress and default risk, which dominated Q2 concerns, have since taken a backseat.

Spread compression in the US market continue to persist, as private credit lenders compete with the syndicated loan market. Market participants say S+450 and S+475 spreads are now common. Among buyout financings, nearly half of private credit loans are priced below S+500.

In a competitive tug-of-war for deal flow, direct lenders captured roughly USD 26bn from the BSL market this year, offset by a comparable flow in the other direction.

Direct lending activity was down in Q3 2025 as M&A activity remains at low levels

Direct Lending estimated volume (US, USD bn) and deal count

Source: HSBC Alternatives, LCD Pitchbook

In Europe, Direct lending activity is set to beat 2024 issuance, with deal count and estimated volume of 117 and EUR 30.5bn, respectively. This is compared to 85 transactions and EUR 25.1bn issuance in the same period in 2024. Spreads in the region continue to tighten – c.64 per cent of LBOs in 2025 have been priced below 550 bps.

European lenders are steering towards the lower mid-market space, with buyouts also showing a trend towards smaller transactions. There were many more buyouts funded by direct lending (17) than by broadly syndicated loans (6) in Q3. However, larger buyout deals went to the BSL market in Q3, leading to a higher volume (EUR 5.6bn from the BSL market).

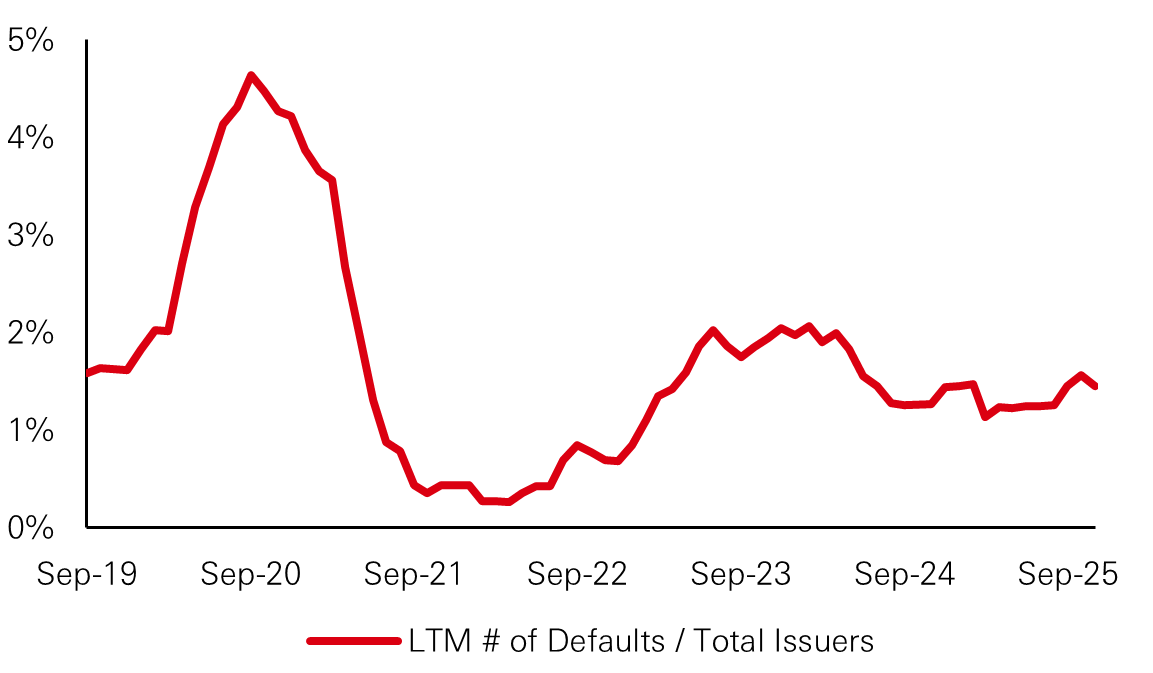

Default rates remain resilient

Leveraged Loans Index Default Rates

Source: HSBC Alternatives, LCD Pitchbook

12-month outlook

Investor demand for private credit remains strong, including inflows from the wealth channel for open-ended products, bolstered by the asset class’s relative stability and yield premium over public markets combined with regular income derived from underlying interest payments.

Deployment and origination of transactions remains the industry’s top challenge, resulting in continued spread compression and slower pace of deployment. Furthermore, regulatory scrutiny for Private Credit will increase as the asset class continues to grow.

Although default rates continue to remain low by historical standards, modest credit deterioration may persist, but proactive equity sponsor support combined with lender flexibility should contain a broader fallout.

During periods of stress, sponsors are expected to rely heavily on tools allowing for flexibility— including PIK toggles and extended maturities — to navigate rate volatility and borrower-level headwinds. Further rate cuts in 2026 could continue to ease pressure on borrowers and further revive deal activity, positioning experienced lenders for attractive, risk-adjusted returns.

Private Equity

Neutral/Positive

Review of Q3 2025

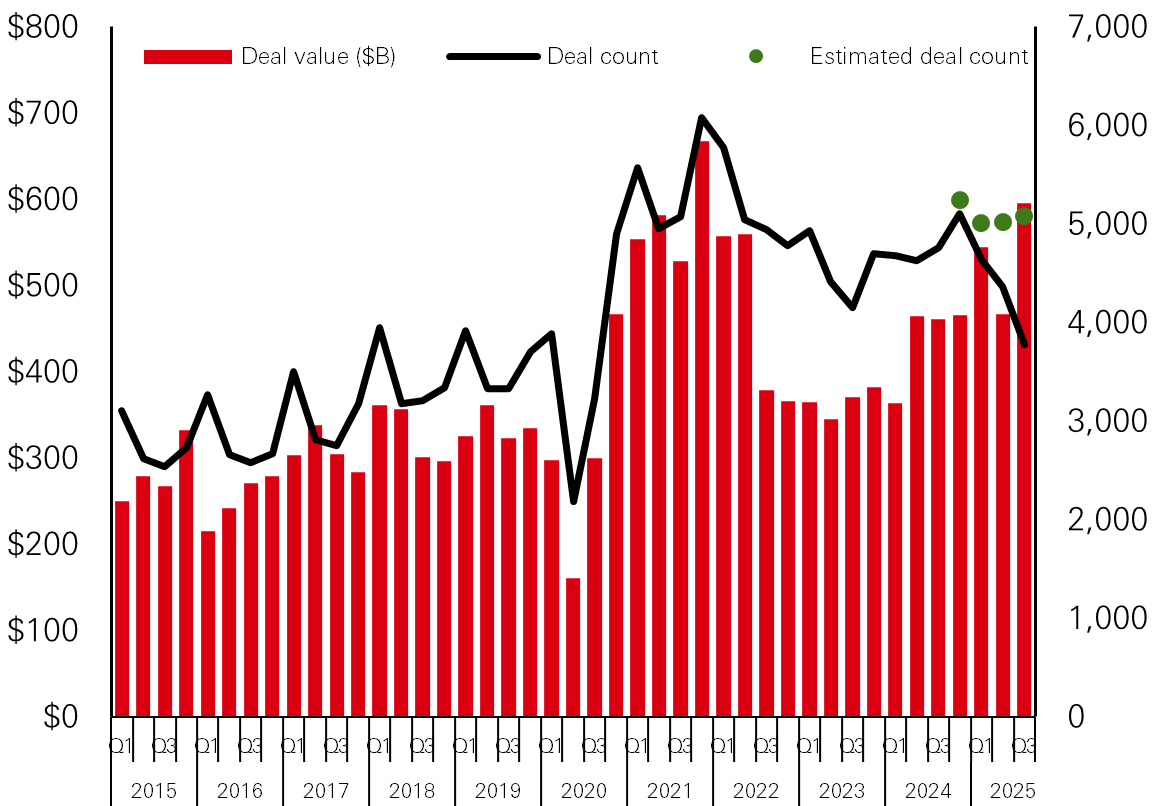

There was a marked pick up in global deal activity in the third quarter of 2025 as market uncertainty over tariffs and US policy subsided. Global deal value was up 27.7 per cent from Q2 levels and up 129 per centover year, and these numbers may rise as data comes through. Growth was mainly in leveraged buyouts and, in terms of sectors, deal value in technology was up 90 per cent over the quarter, driven by a record c USD 55bn deal to take US video game company Electronic Arts private.

Deal count increased marginally over the quarter implying that the large-cap USD 1bn+ deals continue to dominate.

Global PE deal activity by quarter

Capital Invested (LHS), Deal Count (RHS)

Source: HSBC Alternatives, Pitchbook

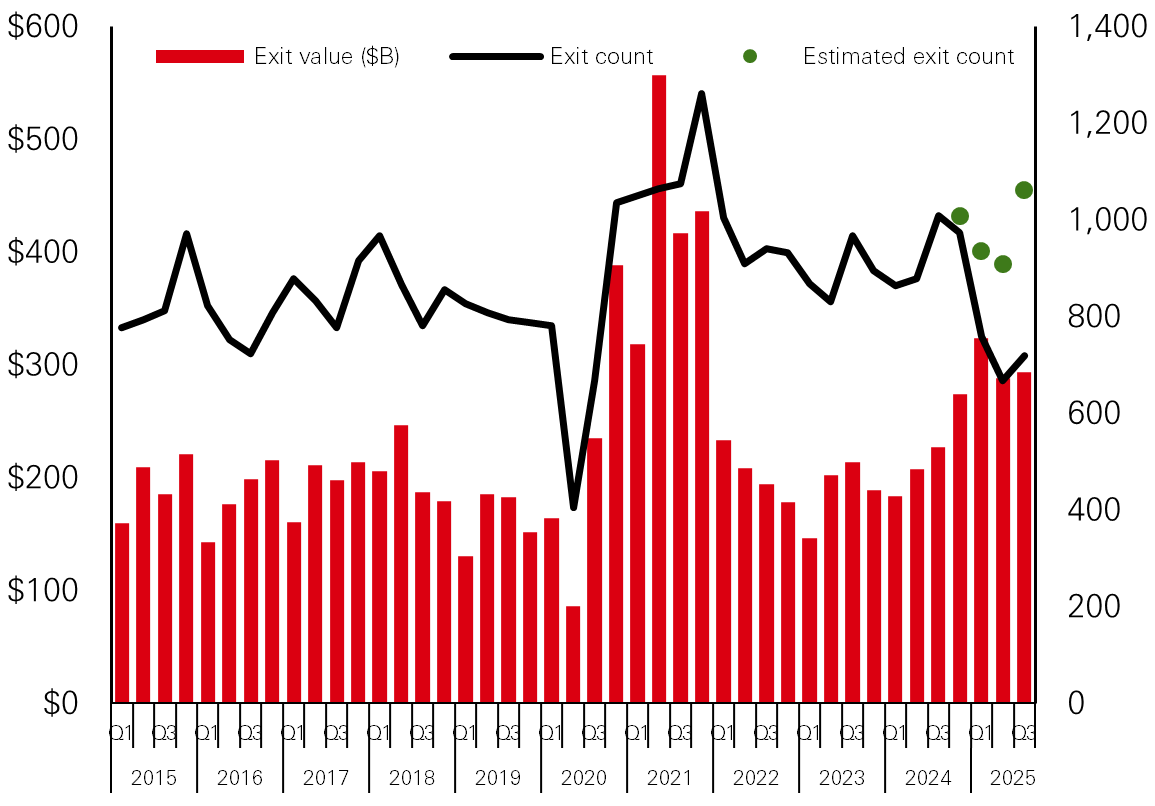

Global PE exit activity by quarter

Exit Value (LHS), Exit Count (RHS)

Source: HSBC Alternatives, Pitchbook

Q3 2025 saw a small increase in exit value of 2 per cent from Q2 levels and up 29.5 per cent over the year. This is a positive development, although a continued rise in exits will be required to materially ease the existing backlog of deals. Growth in exit value was concentrated in Europe, which saw an almost doubling of exit value, and Asia, where exit value rose 53 per cent. The number of exits was up 16.8 per cent in Q3 indicating more assets are moving through the system.

Encouragingly, traditional exit routes-IPOs, M&A and strategic sales are strengthening as confidence returns to the market. GP-led secondaries (continuation vehicles) are also an increasingly attractive route for investors to generate partial or full liquidity.

12-Month Outlook

As we approach the end of 2025, the outlook for private equity has improved amid falling intertest rates and a more conducive market environment. Equity indices remain at elevated levels, exit activity continues to pick up, and the IPO window is showing signs of sustained reopening, particularly in technology and healthcare. The Federal Reserve has cut rates twice to the 3.75 per cent - 4.00 per cent range, and markets anticipate further rate cuts in 2026, offering relief of financing costs. However, the US government shutdown has likely hurt economic growth and delayed the release of key economic data on inflation and jobs, complicating Federal Reserve policymaking.

Tailwinds

- Rate Relief - With the Fed cutting rates in September and October, financing conditions for buyouts and refinancings are materially improving.

- Exit Rebound - Elevated equity markets are helping to reopen IPO and trade sale channels, particularly in technology and healthcare portfolios.

- Corporate Earnings – Technology and industrial sectors reporting solid earnings, pointing towards overall market resilience.

Headwinds

- Rate Uncertainty – The US government shutdown has delayed release of critical market data, creating uncertainty around future rate cuts.

- Policy & Geopolitical Risks – Ongoing political tensions and policy shifts continue to contribute to market volatility.

Real Estate

Positive

Review of Q3 2025

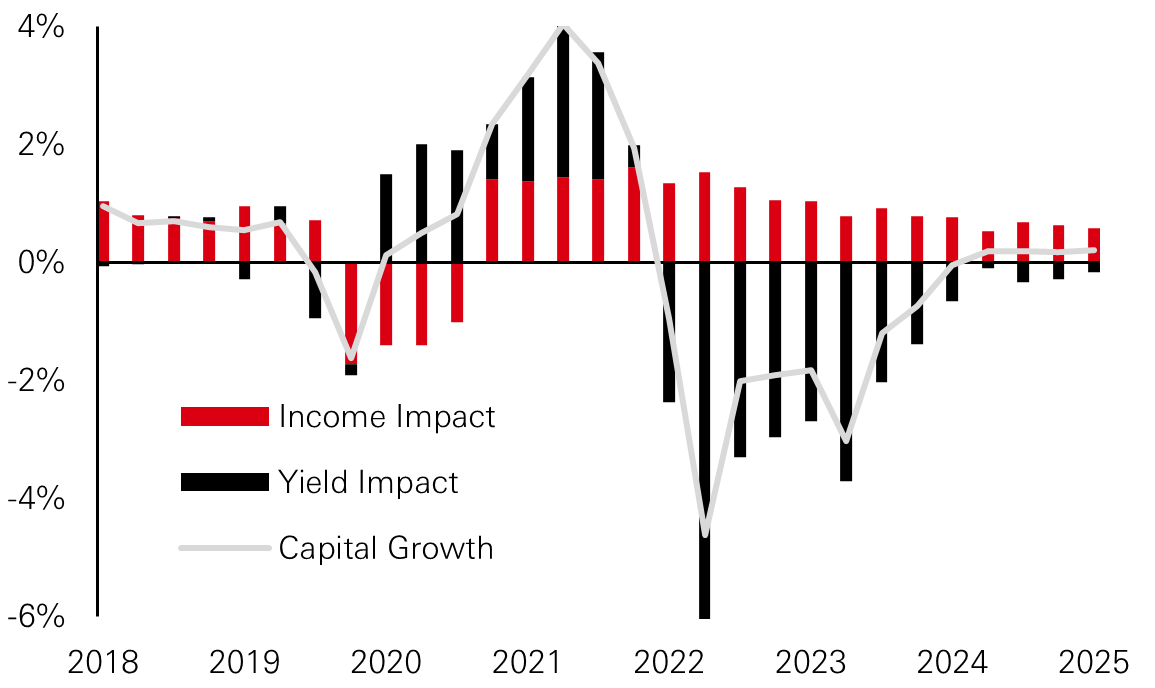

Having declined by 16 per cent between 2022 and 2024, global capital values have modestly increased for four consecutive quarters, according to data from MSCI. In Q3 2025, capital value growth amounted to 0.2 per cent due to ongoing income growth. There is evidence of investment liquidity improving as a moderating supply backdrop has boosted rental growth projections. Moreover, interest rates have fallen, and lending spreads are tightening, especially for high quality assets.

Globally, office vacancy rates remain high, though there were signs of stabilisation in Q3 as tenants look to secure Grade A space in an environment where new development is falling sharply. For example, year-to-date (to Q3) leasing in Manhattan has been significantly above the long-term average, contributing to a decline in the vacancy rate, and healthy prime rental growth. Similar trends are being seen in other global cities such as London, Paris, and Tokyo where demand for modern, sustainable buildings is strong.

Although MSCI reported retail vacancy rates softening in Q3, property fundamentals for prime retail assets are in good health with landlords reporting strong leasing demand from retailers, and near record short watchlists. Landlords of grocery-anchored open-air shopping centres with tenants focused on services (health and fitness, casual dining) are reporting particularly strong sales comps, strong tenant demand and the ability to raise rents. Prime high streets in cities with strong tourism flows, such as Tokyo’s Ginza or Madrid’s Gran Vía, are also benefiting from a rebound in footfall.

Logistics vacancy rates remain in a soft patch as a recent wave of new supply continues to weigh on vacancy rates, though there are signs of improved leasing and slowing completions. The US vacancy rate appears to have stabilised at 7.1 per cent (C&W) in Q3, slightly above pre-pandemic levels. In Europe, rates are declining in the UK and Eastern Europe but rising in France and Germany. Asia-Pacific remains more varied, with tight conditions in Sydney and Melbourne but weaker fundamentals in Singapore (trade uncertainty) and Tokyo (significant new supply).

The residential sector continues to record the lowest vacancy rates globally, according to MSCI, although the US multifamily vacancy rate rose to 4.4 per cent in Q3 (CBRE), predominantly due to supply related softness in the Sun Belt, whereas coastal metros have been relatively more resilient, with notable strength in San Francisco. In Europe and Asia, a widespread lack of development and ongoing structural demand continue to support firm fundamentals for living sectors, for example in Tokyo’s Central 23 Wards the vacancy rate fell to 3.9 per cent (Savills), with strengthening rental growth.

Income continues to underpin capital growth

Decomposition of Global Capital Growth (per cent Q-o-Q)

Source: HSBC Alternatives, MSCI data to Q3 2025

12-Month Outlook

The rebasing of property yields to materially higher levels has created a more favourable outlook for total returns, though with elevated interest rates the risk premium remains to the lower end of historic ranges. Capital value growth will be driven by rental income rather than yield compression while above target inflation keeps interest rates elevated, and yield spreads remain tight. Rapidly declining new supply and tenant preference for new space should support steady rental growth for prime assets across all property types.

Retail yields, which had been rising prior to the pandemic, offer a positive spread over office, logistics and residential yields, whilst a decade of minimal new supply and resilient leasing demand point to stable retail rental growth. Given the fragile economic outlook, assets with a non-discretionary focus should outperform, though “A” malls in affluent neighbourhoods and prime high street retail in strong tourist cities should perform well. Secondary retail will remain challenging.

While the structural tailwinds for logistics property remain intact – e-commerce, reshoring, supply-chain resilience – 2026 rental growth is expected to moderate as recent new supply weighs on fundamentals. As the supply pipeline fades, fundamentals should gradually improve as we move through 2026, particularly in high density, supply constrained urban markets.

The office sector is expected to remain particularly bifurcated, with subdued overall demand but prime assets in global cities benefitting from strong demand and limited new supply. Gateway markets such as New York, London, and Tokyo should outperform. For markets such as Hong Kong and San Francisco, which have been under particular pressure over recent years, but have possibly bottomed in 2025, are expected to continue their recovery, though negative rental reversions will continue to pressure landlord incomes in 2026.

The living sector’s outlook remains resilient, supported by stable cash flows, low vacancy, regular marking to market of rents resulting from short leases, and structural demand drivers such as urbanisation. For US multifamily, coastal markets should continue to outperform the Sunbelt, although we expect the latter to stabilise in the coming 12-months. Stronger performance may be found in Asia, for example Singapore where household incomes are rising strongly or Tokyo where strong urban demand and a lack of new supply is sustaining rental growth.

Slowing development could reduce current vacancy rates

Global Vacancy Rate (per cent)

Source: HSBC Alternatives, MSCI, data to Q3 2025

Infrastructure

Positive

Review of Q3 2025

Q3 saw continued steady performance from evergreen infrastructure funds, with annualised returns across the industry in the range of 7-12 per cent.

According to IJ Global, infrastructure funds that reached final close in the first 3 quarters of the year (to the end of September 2025) raised USD 175.95bn, a 91 per cent increase compared to the USD 92.13bn raised in Q1-Q3 2024. In Q3 2025 alone USD 57.51bn was raised. We consider that this continuing fundraising momentum is illustrative of the attractiveness of infrastructure as a stable asset class in an overall investment universe that faces significant challenges.

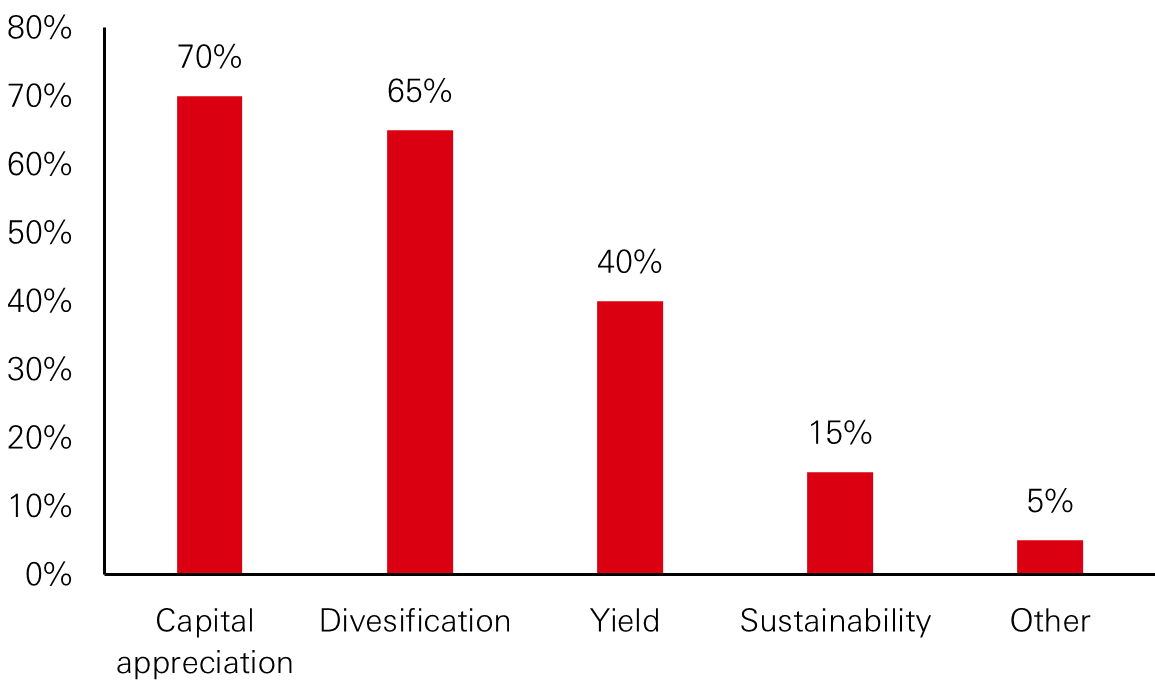

The placement agent Campbell Lutyens has surveyed the reasons why Limited Partners make an allocation to private infrastructure equity. Historically, infrastructure has been seen as a source of yield and as a diversifier within a wider alternatives allocation. The survey results show that capital appreciation has become the primary reason for allocating to infrastructure alongside its portfolio diversification benefit. The capital appreciation objective helps explain the growing preference among infrastructure LPs to invest in value-add infrastructure funds.

Reasons for Infrastructure allocations in portfolios

Campbell Lutyens Survey

Source: HSBC Alternatives, Campbell Lutyens

12-Month Outlook

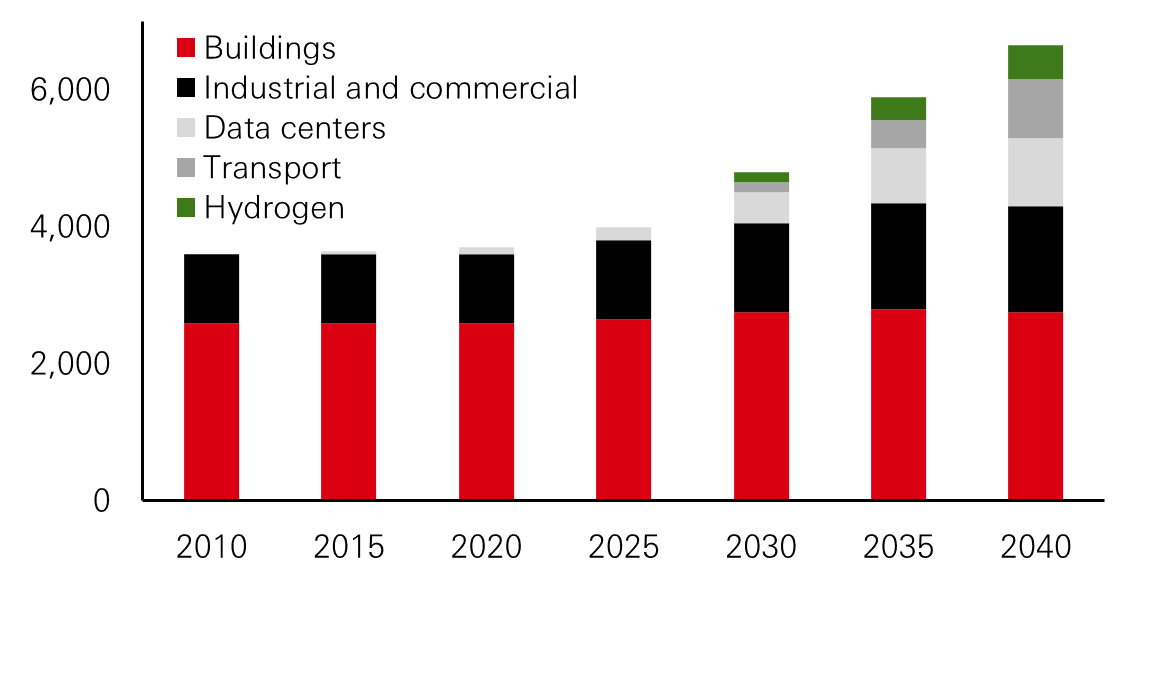

Digitalisation and electrification remain the dominant themes in infrastructure investing. The extent to which these themes interact is partially illustrated in the chart below, forecasting the future growth of electricity in the United States1. Having been flat for decades, electricity consumption is forecast to increase by 3.5 per cent p.a. The principal drivers of this growth are the electrification of industrial production, significant expansion of the data centre segment, and electrification of transport.

Significant Growth expected in US power demand

Decomposition US power demand by sector (terawatt-hours)

Source: HSBC Alternatives, US Energy Information Administration (EIA)

We see multi-sector, digital, and energy and climate transition infrastructure funds following the commercial logic of projected demand for electrification by investing in a variety of existing and emerging infrastructure sub-sectors which are associated with satisfying the demand for new power sources. Some are longstanding such as investments in extending and hardening of electricity transmission networks and the delivery of ever more solar and wind powered energy generation and associated battery storage systems.

Other sub-sectors have emerged relatively recently, including:

- Electrification of buses and commercial vehicles;

- Providing dedicated behind the meter power sources to power new data centres;

- Development of powered land to be sold to data centre developers;

- Building and contracting vessels to construct and support offshore wind farms;

- Buying existing onshore wind farms nearing the end of their operating lives with a view to repowering with new turbines to deliver additional energy production capacity;

- Buying existing peaker gas turbines and developing renewable energy and battery storage assets on the same site to make more effective use of the site’s electricity transmission capacity.

All of these emerging sub-sectors offer the potential to generate significant revenue growth, supporting the delivery of value add (12-16 per cent net) infrastructure returns.

The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target. Past performance does not predict future returns. Diversification does not ensure a profit or protect against a loss. This information shouldn't be considered as a recommendation to invest in the specific sector mentioned.

1US Energy Information Administration (EIA), McKinsey & Co.

Sources: HSBC Asset Management, Campbell Lutyens, as of December 2025; LCD, Pitchbook, as of November 2025; MSCI, CBRE, Bloomberg, as of September 2025.

Important information

Risks of investing in Private Markets

The value of investments and income from them can go down as well as up, meaning you may not get back the amount invested, and you may lose some or all of your investment. Past performance information presented is not indicative of future performance. The return and costs may increase or decrease as a result of currency fluctuations.

- Alternative Risk - There are additional risks associated with specific alternative investments within the portfolios; these investments may be less readily realisable than others and it may therefore be difficult to sell in a timely manner at a reasonable price or to obtain reliable information about their value; there may also be greater potential for significant price movements

- Liquidity Risk - Investors may be unable to dispose of an investment quickly or at all and at a price that’s closely related to recent similar transactions, if any. There is no guarantee of distributions and secondary market is expected to be established

- Event Risk - A significant event may cause a substantial decline in the market value of all securities

- Long-term Horizon - Investors should expect to be locked-in for the full term of the investment, which is subject to extensions

- No Capital Protection - Investors may lose the entirety of invested capital

- Unpredictable Cashflows -Capital may be called and distributed at short notice

- Economic Conditions - Ability to realize/divest from existing investments depends on market conditions and the regulatory environment

- Risk of Forfeiture - Failure to make call payments could result in forfeiture of commitment, including invested capital, without compensation

- Default Risk - - In the event of default investors risk losing their entire remaining interest in the vehicle and may be subject to legal proceedings to recover unfunded commitments

- Reliance on Third-party Management Teams - Underlying investments will be managed by various third-party management teams that will in aggregate determine the eventual returns for the investor, if any

Disclaimer

Important information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets. Investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

This document provides a high level overview of the recent economic environment. It is for marketing purposes and does not constitute investment research, investment advice nor a recommendation to any reader of this content to buy or sell investments. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination.

All data from HSBC Asset Management unless otherwise specified. Any third party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group). The above communication is distributed by the following entities:

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only, and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- in Bermuda by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- in Chile: Operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- in Colombia: HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- in France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- in Germany by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- in Hong Kong by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This video/content has not be reviewed by the Securities and Futures Commission;

- in India by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- in Italy and Spain by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- in Malta by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- in Mexico by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- in the United Arab Emirates, Qatar, Bahrain & Kuwait by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Securities and Commodities Authority in the UAE under SCA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence

- in Peru: HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- in Singapore by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments;

- in Taiwan by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- in Turkiye by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations

- in the UK by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- and in the US by HSBC Global Asset Management (USA) Inc. which is an investment adviser registered with the US Securities and Exchange Commission

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy

Copyright © HSBC Global Asset Management Limited 2025. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Global Asset Management Limited.